Key takeaways:

- The IMF projects the Philippine economy will grow by 5.8% in 2024 and 6.1% in 2025, reflecting resilience despite global challenges.

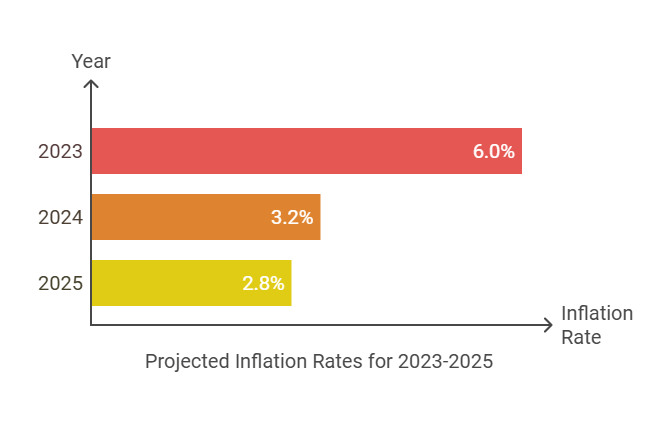

- Inflation is expected to decrease from 6.0% in 2023 to 3.2% in 2024, aided by lower food prices and reduced rice tariffs, providing relief to consumers.

- The IMF warns of ongoing risks such as volatile commodity prices, geopolitical tensions, and stalled reforms that could disrupt economic progress.

- The IMF advises the Philippine government to pursue fiscal consolidation to reduce deficits and debt while ensuring that low-income households are not disproportionately affected by new tax measures.

- There is a call for investment in education and skills development to address structural gaps and leverage the country’s young workforce for sustainable growth.

The International Monetary Fund (IMF) recently praised the Philippine economy for its resilience and growth, projecting the country’s economic growth at 5.8% in 2024 and 6.1% in 2025.

But behind the positive numbers lies a challenge: balancing economic growth with the everyday struggles of Filipinos, like rising prices and limited access to jobs, education, and healthcare.

IMF’s assessment—bright spots and risks

In its December 4 Article IV Consultation, the IMF highlighted the country’s recovery from global challenges, commending measures to control inflation and manage public debt.

“The authorities have handled the challenges arising from multiple external headwinds well with wide-ranging plans for high and inclusive growth,” the IMF said.

Inflation in the Philippines is expected to drop from 6.0% in 2023 to 3.2% in 2024, helped by lower food prices and other non-monetary measures like reduced rice tariffs.

The IMF predicts inflation will settle at 2.8% in 2025, providing some relief for struggling consumers.

Even with some good progress, there are still risks hanging around. The IMF pointed out that global issues like fluctuating commodity prices, geopolitical tensions, and natural disasters could throw a wrench in the works.

They also mentioned that stalled reforms and slowdowns in key trading partners could be potential threats to the economy. So, while things are looking better, it’s important to stay aware of these challenges that could disrupt growth moving forward.

Fiscal consolidation—a tough balancing act

The IMF advised the government to push forward with fiscal consolidation—reducing deficits and debt—to create more room for priority spending. They suggest adding new tax measures, improving tax collection, and tightening controls on tax incentives.

While these steps aim to fund essential sectors like education and healthcare, critics warn they might burden taxpayers already struggling with inflation.

“Additional tax measures should be considered to create more space for spending in priority areas,” the IMF noted in its report.

Economists say these efforts must ensure low-income households are not hit the hardest, as cuts to social programs could worsen poverty.

Monetary policy and inflation concerns

The IMF backs the Bangko Sentral ng Pilipinas (BSP) in its gradual easing of monetary policy to lower borrowing costs and boost economic activity. But it urged caution.

“With inflation and inflation expectations returning towards target, a continued gradual reduction in the policy rate is appropriate,” the IMF said, stressing the need for a data-driven approach to avoid fueling inflation.

Some experts warn that cheaper loans could lead to higher prices, eroding savings and straining household budgets.

“The BSP will need to adopt a data-driven and cautious approach to ensure that monetary policy easing doesn’t backfire,” said a financial analyst in Manila, who prefers to remain anonymous.

Structural gaps and economic challenges

The IMF highlighted the need to address issues like the Philippines’ fragmented yield curve, which complicates borrowing and interest rate management.

They also pointed to vulnerabilities in the agriculture sector and heavy reliance on imports for food and fuel, which make the country prone to supply-driven inflation.

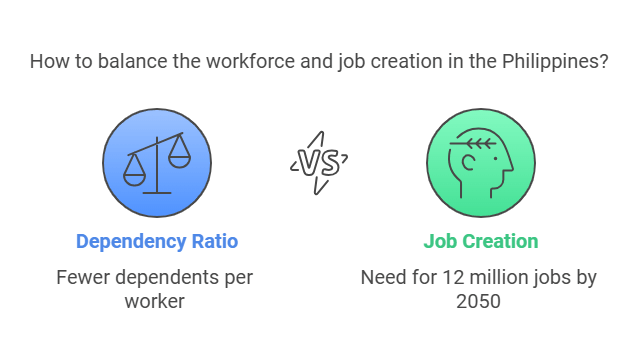

The Philippines’ dependency ratio is projected to fall below 50% by the end of 2024. This means there will be fewer dependents (people younger than 15 or older than 65) for every 100 working-age people (between 15 and 64).

The country will need to create at least 12 million new jobs between now and 2050 to accommodate its rising working-age population.

To capitalize on its demographic dividend—a young, working-age population—the Philippines must invest in education and skills development.

The IMF called for stronger technical and vocational training, better access to higher education, and lifelong learning to build a more competitive workforce.

Financial system and reforms

The IMF has praised the Philippines for making solid progress in fighting money laundering and terrorism financing. They highlighted that the country has largely completed its action plan from the Financial Action Task Force (FATF), which is a big step forward since the Philippines had been under increased monitoring.

However, the IMF stressed the need for reforms to bank secrecy laws to improve oversight and enhance financial stability. While the progress is encouraging, these changes are crucial to ensure that the financial system remains secure and transparent.

Moving forward by balancing growth and well-being

While the IMF’s recommendations aim to sustain economic growth, the government faces the challenge of ensuring these policies do not hurt everyday Filipinos. Achieving this balance will require thoughtful policymaking to protect the vulnerable while driving long-term progress.

The road ahead is clear: sustainable growth in the Philippine economy must go hand-in-hand with improving the lives of its citizens. Whether this balance is achieved remains to be seen.Ⓒ

Leave a comment